Ah CPF, the grand retirement plan set out for all of us, each step of the way predefined. There’s nothing much to do about it right? So keep chucking that 20% of your salary in there and just wait till 65

lor, the government has it all settled for us.

What if I told you we could commit a small act of rebellion, and hack the growth of our CPF money? While still playing by the rules of course.But before that, one has to first understand how CPF works when you turn 55.

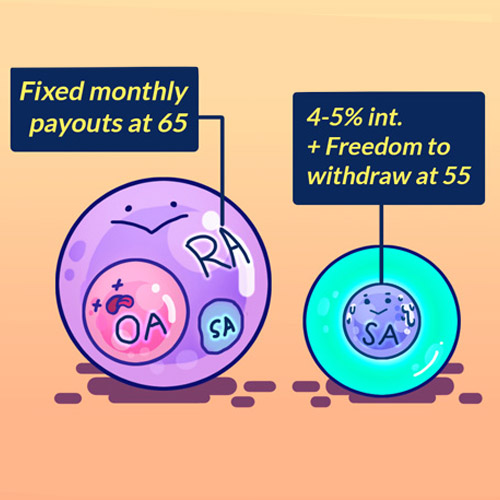

At age 55, our Retirement Account (RA) will be created, in order to fund CPF monthly retirement payouts that begin at age 65. The RA is formed by money funnelled from both our SA and Ordinary Accounts (OA).But the key concept to understand is that to fund the RA sum, money from our SA account will be drawn on

first before our OA money follows suit.

“Who cares?” you say, but here’s why you should: After the RA is formed at 55, any excess money that remains inside your SA or OA can be withdrawn, either partially or even all at once.

But realistically speaking, our SA accounts will likely be depleted during the RA’s formation, this means any money left to withdraw upon will likely be in our OAs.

With the SA interest rate being a whopping 4-5% while the OA rate is 2.5% – 3.5%, wouldn’t it be great if we could leave more in our SA?

Here’s where we get into the SA shielding hack.

How To Shield Your SA Funds

It’s simple, really. The key to the hack is to transfer your SA money out of the account with the CPF Investment Scheme (CPFIS) before the money is funnelled away to the RA at 55.

How you can do this is by searching for low-risk investments to channel into — ideally, Treasury Bills or Singapore Government Securities bonds (not the same as SSB), both of which are as low-risk as you can get. These are government-backed investment instruments with short investment periods.

Note that the first $40,000 of your SA account cannot be used for investments.

Here’s more information on these two investment instruments:

| Investment Instrument |

What They Are |

Tenor Period |

| SGS Bonds |

Government-backed bonds with a fixed interest rate |

2 years to 30 years |

| Treasury Bills (T-Bills) |

Short-term securities issued at a discount of face value; upon maturity, investors will receive the full face value |

6 months to 1 year |

Remember: The shorter the tenor period the better, because it means you won’t have to wait long after you turn 55 (if you time it right) to transfer your money back into the SA, so the money enjoys the sweet, sweet 4-5% interest rate.

Why SA shielding?

After turning 55, there is no way you can top up your SA again, so leaving as much money in a

guaranteed, no-risk, 4-5% yielding account — that you can slowly withdraw upon — is a priceless financial tool.

Will the government plug this gap by the time most of us turn 55? Perhaps.

But this is

still useful information for those with parents who are turning 55 soon. After all, for young working Singaporeans, being caught in an inter-generational sandwich is a real issue. So helping your parents have the tools to achieve a self-sufficient retirement will have a very real impact on your own wallet!