Financial Planning | Investing | Life | Personal Finance | Personal Stories | Article

The Money Moves I Wish I Made in My 20s

by Regiena R. | 21 Mar 2022 | 12 mins read

This article is brought to you by Standard Chartered Bank’s JumpStart Account.

Our 20s are a time of great possibility. It’s when we step into adulthood, venturing bright-eyed and full of energy into the working world.

And with our new jobs, we’re suddenly flushed with more cash than we’ve had before. Getting our paycheck for the first time sure beats the measly allowance we’ve been getting from our parents!

I was a broke student while I was studying, so to have a four-figure amount seemingly magically appear in my bank account every month was both novel and exciting.

All the things I could do with that money, I thought to myself.

The upscale restaurants that I’ve always wanted to dine in wasn’t far out of my reach anymore. Every so often, I’d treated myself to vacations too. I splurged on things that seemed like necessities back then such as clothes, shoes and bags that were on sale.

The initial euphoria that came with spending money frivolously wore off eventually. In its place, dread and anxiety set in as I saw my bank account go dangerously low before my next paycheck came in every month. It also didn’t help that there were several large expenses that I had to take into account for — from small, unexpected expenses such as cracked phone screens to big life decisions such as contemplating quitting a job.

I soon realised that spending every single cent from my paycheck every month didn’t give me the freedom to make life decisions — big and small — without fear. Looking back, I could have saved myself a lot of stress and hassle had I made better money decisions in my 20s.

Here’s what I would do differently if I could do over my 20s.

When it comes to savings, aim sky-high

In my 20s, I had almost zero financial commitments. I was single and living at home with my parents. If I just tried a bit harder, I could easily saved almost 70% of my income each month.

Every now and again, my parents would advise me to save. But back then, I couldn’t fathom depriving myself of bubble teas, staycations, and dinners out. After all, I worked hard to earn that money, shouldn’t I get to use it?

It was a little late but I later learned that saving as much money as we can in our 20s set us up for an easier and more fulfilling life in our 30s and beyond.

Admittedly, we tend to be short-sighted in our 20s, only thinking about what’s right in front of us. But as we get older, we inevitably have to make significant life decisions – getting married, buying a house, changing jobs, moving to a new city, or going back to do a masters. All these will require lots of planning and money.

Related

")

Many of us only start saving when our goals feel more tangible and immediate, and the process of saving up for them can feel overwhelming, especially when they require a hefty amount, and we want to achieve them within the timelines that we set for ourselves.

So, it pays to save up as much as we can as early as we can, even when we haven’t really thought about the goals that we want to achieve. It may seem pointless when you’re not saving for a specific purpose but honestly, the hardest part of saving money is often just getting started.

In my case, I wanted to hack my brain into thinking I had much less money than I really had each month in my bank account to spend, so I set up a standing instruction to put 50% of my salary each month into a high-yield savings account that I don’t touch.

I did feel the pinch when I started saving half my income, but I adapted to spending lesser.

Don’t just save, invest it too

If I could impart a game-changing advice to my 24-year-old self, it would be this: If you save and invest as much as you can as early as you can, you could stop setting aside extra money to invest altogether (if you wanted to) for the rest of your life and you’d still be able to build wealth for decades to come.

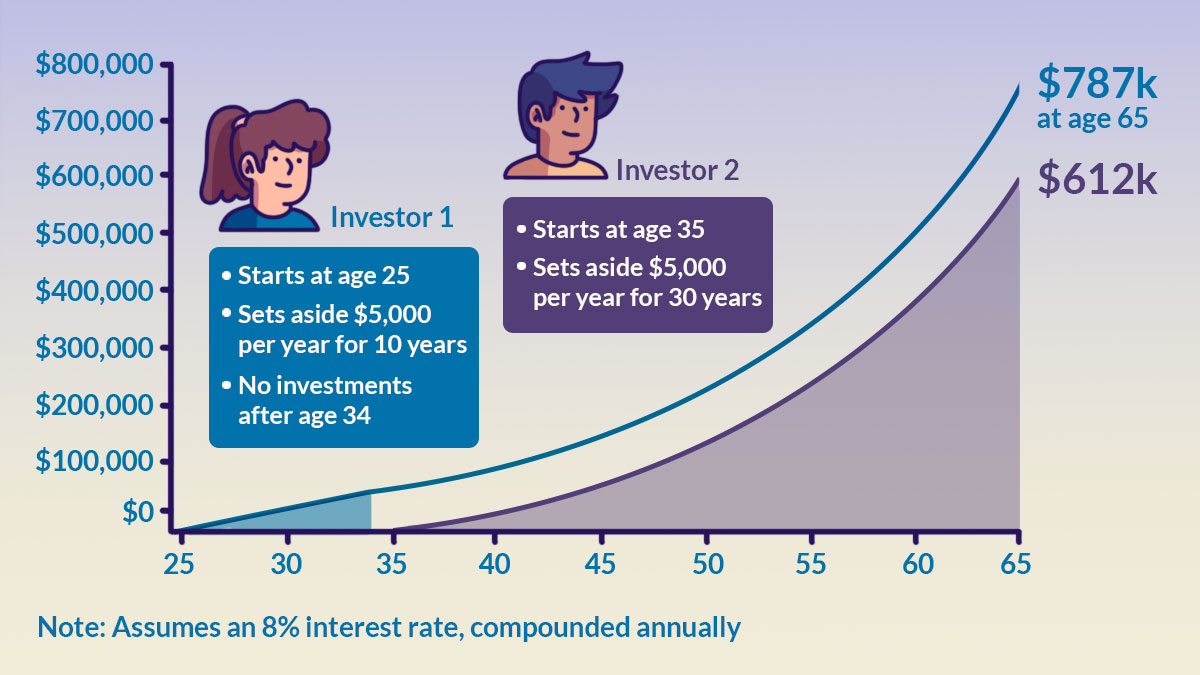

What do I mean by this? Well, let’s take two people who decided to take different investing approaches. At 25 years old, Investor 1 invests for only the first 10 years of her working life and then stops at age 35. Investor 2 decides to start investing at age 35 and continues investing for the next 30 years. Assuming both set aside $5,000 a year for the duration of their investment and they earn 8% a year on their money, who do you think ends up with more money when they hit age 65?

Believe it or not, the answer is Investor 1.

In short, if you started investing in your 20s for only 10 years, you’d end up with more money when you retire than someone who only started in their 30s and invested for the rest of their life.

That’s because money invested earlier, even though it’s a smaller sum, grows more than money invested later because of compound interest.

Another key thing to note is that when you start investing later, you’d have to put in more money to play catch up. In the chart above, we can see that Investor 2 invested a total of $150,000 while Investor 1 invested $50,000 and yet, he still ended up with lesser wealth than Investor 1.

And wouldn’t you rather just sacrifice and stay disciplined only for 10 years in your 20s than to have to do the same for rest of your adult life?

So, don’t just save aggressively in your 20s, make sure to set aside some of that savings into investments too.

Quit playing the appearance game

I entered adulthood just as the age of the influencer rose to prominence and sharing our lives on social media became commonplace. Suddenly, it wasn’t just celebrities and billboard advertising that would entice us buy things, but everyday people too.

As I scrolled through social media, I’d notice what clothes my peers were wearing, the latest gadgets they bought, which restaurants they dined in, and where they went on vacation. I would feel the urge to emulate their lifestyle and to show them that I too was “living life to the fullest”.

I would say yes to every party, every sale, and every night out. When I got bonuses and pay increments, I didn’t save up that money but instead upgraded my lifestyle. This is also known as lifestyle inflation.

In your 20s, it’s tough to go against the grain when you’re surrounded by people that directly or indirectly make you feel like you need to keep up appearances. But looking back on it, I do wish I learned a lot sooner that maintaining appearances ultimately doesn’t make us feel fulfilled and happy.

Related

This type of lifestyle can cause more stress than enjoyment in life. With no additional savings in the form of an emergency fund or money invested to help us reach our life goals, we come out of our 20s having to start saving from scratch for the life we want to lead in our 30s and beyond.

If I could advise my 20-year-old self, I’d tell her that it’s okay to keep our lifestyle costs minimal and enjoy the simple luxuries of life like going for a walk or staying in on a Friday as self-care.

We don’t need to experience everything all at once while we’re still young. There’s plenty of time to see the world and try new things when we are older.

Focus on growing income to grow wealth

Have you ever spoken to someone older than you who’ve said something like this?

“When I was your age, I had so much more energy to do things!”

Or “It was so much easier to pick up new things when I was younger!”

There’s no denying that we have more energy, time, and our brains are intrinsically more elastic so any new skills we pick up stick faster when we’re younger. This makes our 20s the best time to capitalise on these depleting resources to help us grow our income, whether it’s picking up technical skills that gives us an edge in the workforce so that we can demand a higher pay or working a side-hustle to supplement our day jobs.

To a 20-something-year-old, however, there’s very little appeal in working hard, sacrificing our social life just to earn more money. (I’ve been there!) But earning more money now buys us more freedom further down in life. Having some FU money gives you the courage to walk away from situations that are bad for you such as a toxic job or relationship. In addition, it also gives you the ability to pursue the things you enjoy such as passion projects or taking a sabbatical to travel.

Related

You’d thank yourself when you’re able to bump your starting salary of $3,000 by 50% to 100% with a side hustle and upskilling at your day job. Not only will your income outpace inflation, but you’d also be building wealth a lot faster than just investing alone. And you could make it grow even faster by investing that extra income.

Furthermore, earning more money earlier in your 20s would mean that you can also set aside more money towards your savings to build an emergency fund faster and then go on to save and invest more aggressively for your financial freedom.

It also helps to surround yourself with people who are as equally driven as you to motivate, encourage and support you in your pursuits to grow your wealth.

It starts with the right attitude

The financial moves I’ve mentioned so far – growing income, saving, and investing aggressively, keeping a low-cost lifestyle – is ultimately dependent on your attitude towards money in your 20s. Frankly speaking, I didn’t even want to start thinking about money when I was 20 so it would have been an uphill battle to convince myself to make these financial moves.

However, if I could travel back in time, I would tell my younger self to just get curious about money. Dealing with finances doesn’t have to be a chore. In fact, you could turn it into a game that you play with yourself or do a couple of savings challenges with friends.

The idea is just to get comfortable speaking about money and managing it. And you don’t have to be perfect with it either. Let’s be real, most of us will fumble and make mistakes along the way, but we can afford to learn from those money mistakes when we’re younger, with less commitments and more time to come back from them.

Related

Content sponsored by Standard Chartered Bank

When you’re getting your act together in your 20s, one place you can start putting your savings into is Jumpstart Account.

You will earn the prevailing interest rate of 0.50% p.a. on deposit balance up to S$20,000 in your JumpStart account. You will earn an additional Step Up interest of 0.5% p.a. on balances up to S$20,000 in your JumpStart account when you successfully subscribe through us one or more Eligible Unit Trusts; or set up a Regular Savings Plan; or put through at least one Equities buy order; and settle through any investment account held by you as a primary account holder. Step Up Interest is earned in the calendar month that you complete a buy trade and shall be credited to the Eligible Account by the next calendar month. Your JumpStart account must be linked as the primary account to the Cashback debit card in order for you to earn the 1% cashback on eligible MasterCard spends with your Cashback debit card. No min. spends. T&Cs apply.

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$75,000 in aggregate per depositor per Scheme member by law. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured

This article is being distributed for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article is for general evaluation only, and it has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regards to the specific investment objectives, financial situation or particular needs of any particular person or class of persons. You should seek advice from a financial adviser on the suitability of an investment for you, taking into account these factors before making a commitment to invest in an investment. In the event that you choose not to seek advice from a licensed or exempt financial adviser, you should carefully consider whether this investment is suitable for you.

Find out more here.