Budgeting | Personal Finance | Article

3 Things You Should Budget For That You Don’t

by Ooi May Sim | 18 Oct 2021 | 6 mins read

This article is sponsored by Standard Chartered. Apply now for the new Standard Chartered Smart Credit Card and get a 6-month subscription to Disney+ and 6% cashback on all eligible spend (capped at $200) in the first month.

You open Microsoft Excel, then spend hours logging in all the numbers. From loan repayments and utility fees to grocery bills, you map out where every cent you earn is going.

After calculating all your expenses, you are proud to be able to set aside 20% of your income as savings. Life is good.

Suddenly, you get caught up in a busy work period. You do your job, go about your day, and before you know it, it has been six months since you drew up your budget. Maybe, it is time to plan a vacation. You open your bank account and…JIALAT! Where is all my money?!? I should have more than what there is in my account.

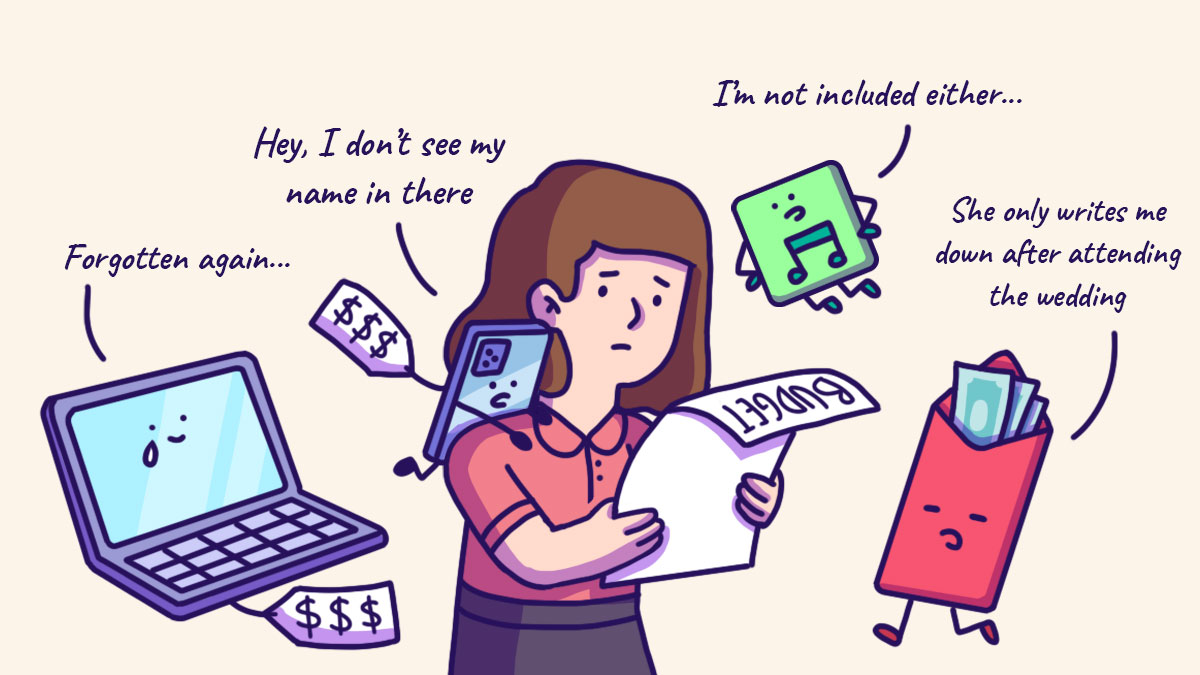

Well…often, the problem lies not in your spending, but with your budget itself. You see, most of us often forget to include some crucial expenses, which can sabotage our otherwise fool-proof plans.

So, what are some common things people often forget to budget for?

Gadgets

Let’s face it. Gadgets these days are not nearly as hardy as they used to be (remember the indestructible Nokia 3310?) Drop a smart phone and chances are, the screen would crack, and you will need to get it fixed, or replaced!

Often, we don’t wait until gadgets are damaged or irreparable before replacing them. You do it when a gadget starts giving you problems, indicating it is close to its shelf life, or if you want a technology upgrade. And most gadgets don’t come cheap.

Because of that, it is essential to factor this into your budget every year.

Pro-tip:

While you may have already accounted for the cost of your gadget in your yearly budget, it’s still going to be hard to see your bank account balance drop by $2,000 every time you upgrade to a new laptop or phone.

If the hefty price tag of a new gadget intimidates you, look for ways to optimise your payments. One option is purchasing your gadget using a credit card that allows you to switch your purchase from a one-off lump sum to an instalment plan. That way, payments are smaller and more manageable each month. Paying $200 a month for 12 months is indeed a lot more predictable and manageable each month, as long as it’s within your means.

Bonus points if you find a card that doesn’t charge you a service fee to convert your payments into an instalment plan or one that gives you cashback on the service fee.

Monthly and yearly subscriptions

When we get home from a tiring day at the office, there’s nothing more relaxing than to kick back and unwind with some cable television. Fortunately, there are tons of options to choose from, such as Netflix, Disney+ and Amazon Prime.

Somehow, these monthly and yearly subscriptions often slip past us, unnoticed, as we tend to sign up for them at different times of the year. To put things in order, write down all the subscriptions you have, or those you plan on getting, the amounts involved and the payment due dates. Plan and budget for them.

Pro-tip:

Find ways to hack your subscriptions and scout for deals out there that allow you to get subscriptions for cheaper, or even free. For instance, saving $12 a month on your Disney+ subscription for 6 months allows you to pocket a total of $72 in a year.

And if you have a credit card that provides rewards or cashback, consider expensing your subscriptions to your card.

P.S. Different credit cards give varying amounts of cashback for different types of spending, so find one that gives you the maximum cashback for the type of spend you’re incurring. Better yet if there’s no minimum spending required to obtain it.

This way, not only do you get to save more, but you’ll also have an overview of all your subscriptions in one place so you can add or cull subscriptions as you see fit.

Related

Special occasions and celebrations

All of us have family and friends, and they all have birthdays. On top of that, there will be, from time to time, other reasons to celebrate too, such as graduations, weddings, and baby showers. Which means it’s time to bring out the Champagne!

Truthfully, most of us don’t think about birthdays or celebrations until they are around the corner, which means we don’t budget for them.

Pro-tip:

If you already have a list of people in mind, make sure you’ve allocated enough money for them to splurge on a coffee date or buy a gift.

Work within your budget and always try to get value for your money. When splurging on a meal for your partner’s birthday, stretch your dollar by looking for rewards and cashback deals, and use a credit card that can allow you to save even more. This gives you more spending power, plus, who doesn’t love getting cashback?!? Remember, the higher the cashback, the more you save.

Related

Content sponsored by Standard Chartered Smart Credit Card

A message from our sponsor:

Expenses keep increasing each year. So, to overcome that, we have to become smarter with our budget and how we increase our savings when we spend. This means looking for credit cards that helps you save more with cashback.

Standard Chartered’s recently-launched Standard Chartered Smart Credit Card allows you to do just that. You’ll get 6% cashback in equivalent Rewards Points, with no minimum spend on your subscriptions, everyday spend at coffee shops and fast-food restaurants, and on your bus or MRT ride. For the first month, cardholders will also get 6% cashback on all eligible spends. So, you’ll get even more savings!

You can also manage your finances with interest-free monthly instalment plans. Convert retail transactions over $200 into 3-month interest-free instalment with 100% cashback on the service fee itself on the EasyPay Instalment Plan.

There are no hidden costs, the annual fees are perpetually waived and the cash advance fees enjoys the same right now.