Over the past two weeks, we’ve kickstarted a series on the odds of you actually using your insurance. Previously, we looked at

term insurance and

health insurance. This time round, we’re diving into critical illness insurance.Throughout this series, we crunched the numbers on the estimated premiums you’ll pay and used some statistics to gauge the probabilities of certain death and hospitalization. (Morbid, we know. But rest assured that it’s for the greater good.)

After all, most people are more paranoid than they’d like to admit. And they definitely worry about being the unlucky few who meet with an unfortunate illness or injury.That’s where we come in — to help you make informed decisions with cold, hard facts rather than mopey, fear-driven emotions.

Let’s get into the nitty-gritty of critical illness insurance.

Part 3: Critical Illness

[caption id="attachment_3369" align="aligncenter" width="300"]

“How critical are we talking here?”[/caption]

What is it?

This insurance offers you a one-time lump sum payout in the event you are diagnosed with a critical illness.

According to the

Life Insurance Association Singapore, 95% of critical illness claims stem from the following conditions: major cancers, heart attack, stroke, bypass surgery and, kidney failure.

How much to pay?

To calculate a monthly amount, the assumptions are:

- 25-year-old male

- Non-smoker

- $100k payout

The average cost you’ll need to pay ranges from

$84.50 – $118 per month.

What triggers the payout?

When you’re diagnosed with a critical illness.

So, how likely will you need critical illness insurance (i.e. what are my chances of being diagnosed with a critical illness in Singapore?)

If we go with the example of cancer, Singaporeans are at a

22.66% risk of being diagnosed with it in their lifetime. That’s more or less one out of four Singaporeans. If you’ve ever wondered what the highest cause of death in Singapore is… it’s cancer.

So with such a high prevalence rate, buying critical illness insurance then seems to be a good investment!

The risk of cancer diagnosis sharply

increases at age 45-54, contributing to 14.1% of new cases of cancer cases.

The risk peaks at

65-74 years old at 25.4%.

This increased risk with age is similar in

kidney failure,

heart attack, and

stroke, where the peak age group of developing these conditions range from 65-70.

Presenting an Alternative:

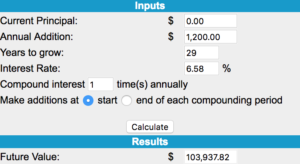

If you had instead invested the average critical illness insurance payment, of $100 every month, in the

STI ETF — a beginner investment vehicle that has generated 6.58% average returns per year since its inception — you would have, by age 54, made $103,938.

[caption id="attachment_3368" align="aligncenter" width="300"]

moneychimp.com[/caption]In other words, you would have outearned the critical illness payout of $100,000

before reaching the age where you’d have the highest chances of developing critical illnesses.

And remember how critical illness works: the insurance company pays you a one-time $100,000 upon diagnosis. The insurer then shakes your hand, and you part ways.

Investment, then, is no different from “self-insuring” and being your own CI insurance plan.

And the kicker? If you manage to dodge the various odds of developing a critical illness, that $103,938 you painstakingly invested for would be yours to pocket.

If not, the total insurance you’ll pay over 50 years will be

$50,700 – $70,800.

But going the “self-insured” route comes with its own conditions:

- Hand on your heart: can you diligently invest the money for 28 years?

- Are you confident the STI (or any other investment strategy) will guarantee that 6.58% return?

But as usual, that’s a risk only

you can decide to take.

Disclaimer

Throughout this series, we found that the chances of utilising some policies look surprisingly small. But before you rage-call your insurance agent and demand a policy cancelation, you have to ask yourself.

“What if I’m the unlucky one?”

For some, having the peace of mind is worth its price tag.

With these statistics we hope to provide you with additional information to a usually fear-driven decision.

Do Also Consider

Do you have:

- A family history of illnesses?

- A smoking habit?

- An existing health condition, such as high blood pressure?

These factors may increase your chances of early mortality, and the cost of your insurance policy.

The figures used in the article are the latest available to us. When we cross-reference datasets from various sources, the data period is standardised to the best of our ability to ensure consistency.