Personal Finance

The Subscriptions You Forgot To Cancel Are Haunting You

I guess that “free” trial wasn’t actually free after all.

28 Jul 2026

READ MORE0

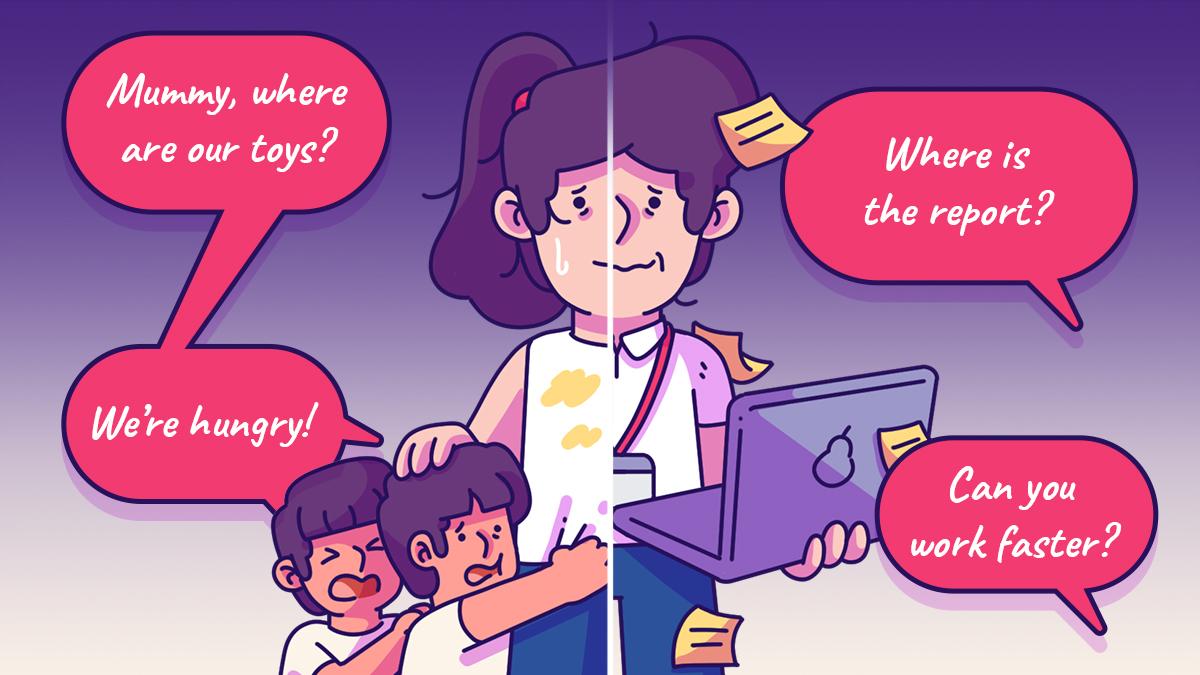

The Things A Working Mum Never Says Out Loud

23 Jul 2026

0

‘Don’t Use Credit Cards Overseas,’ That’s What I Thought Until My Friend Exposed This

22 Jul 2026

0

Low-Effort Ways To Fund Your Next Escape

16 Jul 2026

0

ChatGPT Has Become My Friend, Confidante, And Now Career Coach

13 Jul 2026

0

Job Search Frustration? Here’s How AI Can Lend A Hand

10 Jul 2026

0

I Thought Being A Football Fan Gave Me An Edge In Betting

06 Jul 2026

0

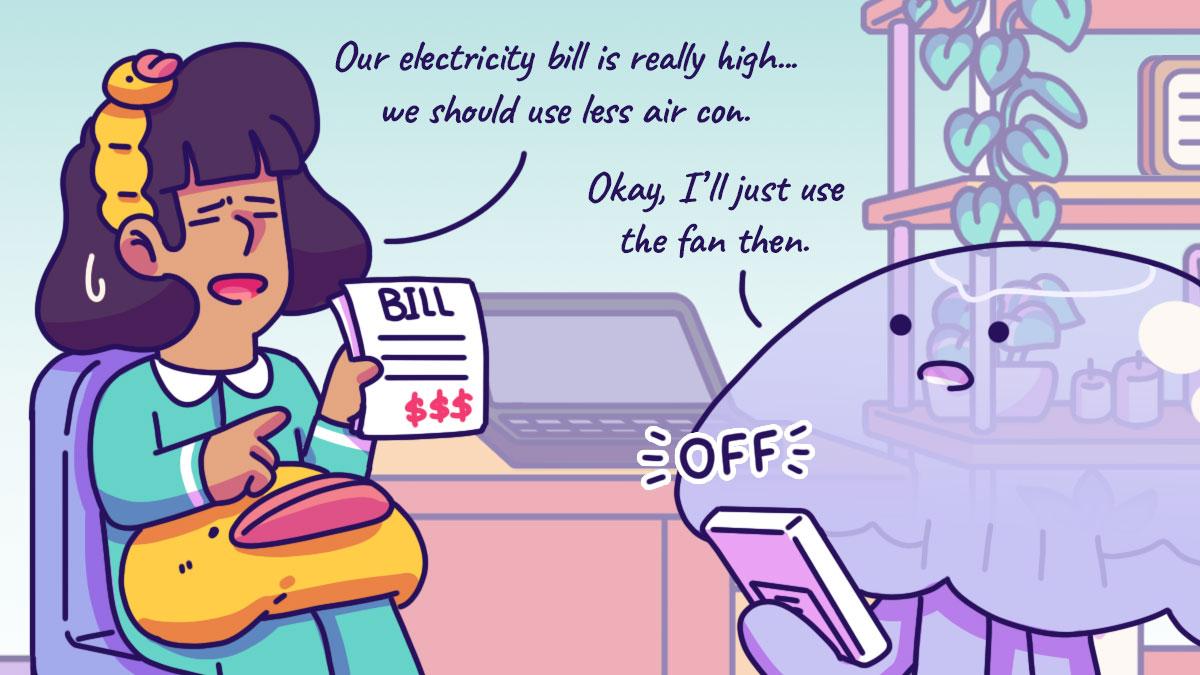

Do You Really Need Air Con?

03 Jul 2026

0

Put An Engagement Ring On It... But Which One?

26 Jun 2026

0

How To Build A Side Hustle Without Messing Up Your Day Job

25 Jun 2026

0

SUBSCRIBE

STAY UPDATED!

And join our community© Copyright 2025 The Simple Sum. All Rights Reserved.