Managing Debt

The First Big Bill I Paid On My Own As An Adult

Turns out free-dom isn’t free. What was your first bill that made your wallet cry?

16 Jun 2026

READ MORE0

I Wished I Learned These Things About Money Sooner

21 Apr 2026

0

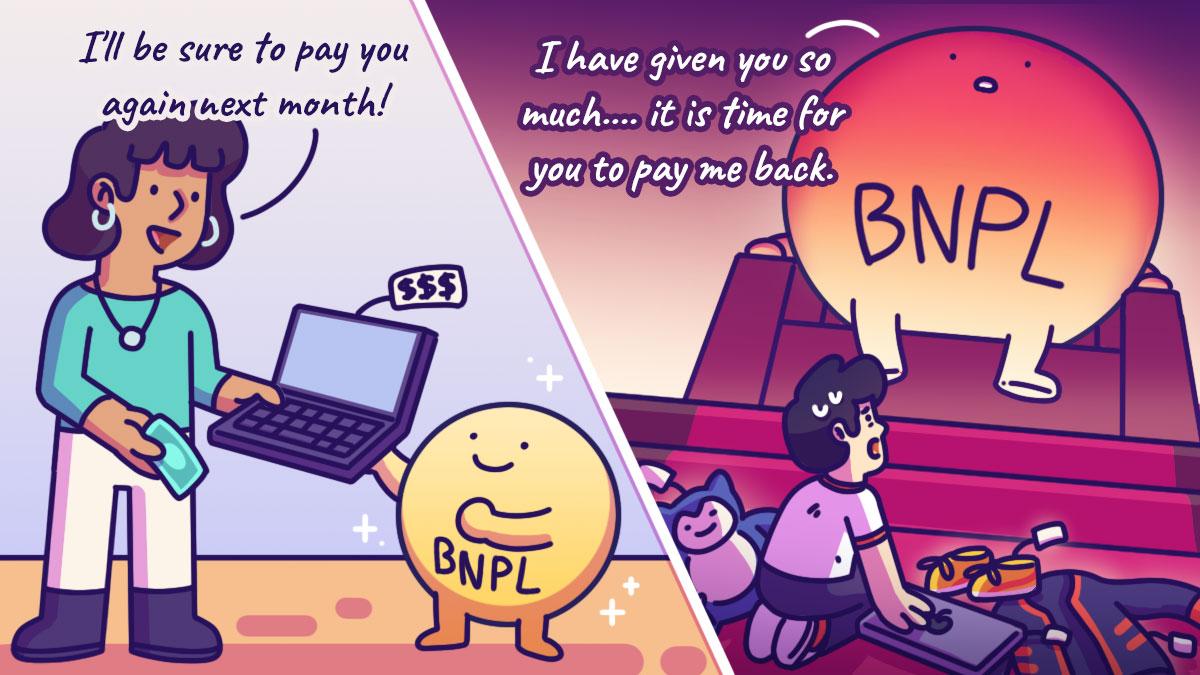

Is BNPL Helping You… Or Hurting You?

04 Mar 2026

0

Are You Ready To Take Your Relationship With Your Partner To The Next Level?

26 Feb 2026

0

Here’s How To Use Credit Without Letting It ‘Use’ You

28 Jan 2026

0

I Ended My Relationship Because He Had 10 Active BNPL Purchases

27 Jan 2026

0

A Millionaire At 39, But Money Didn’t Make Me Happy

19 Jan 2026

0

My ‘Claw Machine’ Addiction Clawed $5K Out Of Me

13 Jan 2026

0

A Christmas Carol That Spooked His Bank Account

23 Dec 2025

0

I Ended Up Borrowing Money From My Parents To Pay For My Buy Now Pay Later Highs

11 Nov 2025

0

SUBSCRIBE

STAY UPDATED!

And join our community© Copyright 2025 The Simple Sum. All Rights Reserved.