Hey dear, want to BTO first?” And with those words, your life changed – better figure out what you’re getting into for a new home.How much can you afford in a new home? How much do buyers need to fork out and when?It’s best to go in prepared. Here are the essentials on buying a new home, before actually buying it. We go through the specific costs you need to pay for a BTO flat.

Eligibility for BTO

Not everyone can apply for a BTO flat – there are a set of requirements to fulfil:

- Applicants must consist of at least one Singaporean Citizen (the other can be a citizen or permanent resident)

- At least one applicant must be 21 or older

- Monthly household income (for 4-room or bigger) cannot exceed $12,000

- Applicants must not own other local/overseas property

- Applicants must not have received more than one CPF Housing grant so far

Grants for BTO

For those eyeing a brand new BTO flat as their first home, there are two main grants to look out for. Bear in mind that these grants are applicable for 4-room or smaller flats in non-mature estates.

Special CPF Housing Grant (SHG)

- Monthly household income does not exceed $8,500

- Grant amount of up to $40,000

Additional CPF Housing Grant (AHG)

- Monthly household income does not exceed $5,000

- Grant amount of up to $40,000

For couples with a monthly household income of $5,000 and below, these two grants can be used concurrently to offset the BTO flat prices.

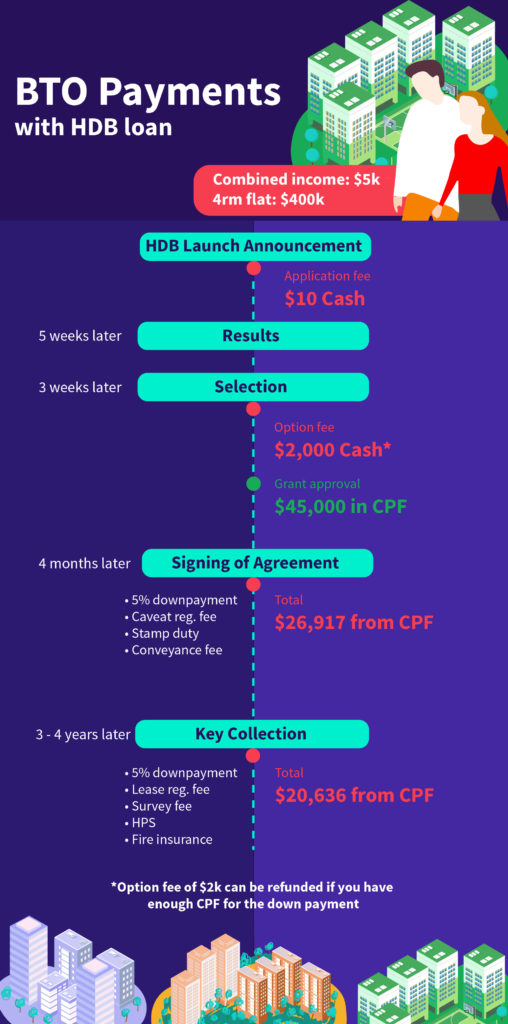

Upfront costs

With the purchase of a new home, one should anticipate upfront costs that cannot be avoided. Ready the wallet for more spending, because these include:

Payable in Cash

Application fee: $10

Incurred when submitting an online flat application

Option fee

- 2-room: $500

- 3-room: $1,000

- 4/5-room and EC: $2,000

With the HDB housing loan, this fee will be refunded if there is enough CPF to cover the downpayment cost

Payable via CPF

Down payment

- HDB housing loan: 10% of flat value

- Bank loan: 25% of the flat value, 5% of which must be paid in cash

Stamp duty

- 1% of the first $180,000

- 2% of the next $180,000

- 3% of the next $640,000

- 4% on the remaining amount

Conveyancing fee

- First $30,000: $0.90 per $1,000

- Next $30,000: $0.72 per $1,000

- Remaining Amount: $0.60 per $1,000

Caveat registration fee: $64.45

Lease registration fee: $38.30

Survey fee: $294.25

Stamp duty on Deed of Assignment (only for bank loans): 0.4% on loan amount, capped at $500

Home Protection Scheme: Calculate home protection costs with

CPF’s calculator

Fire insurance: $1.50 to $7.50 per 5-year term

Owning a home in Singapore is never too far out of reach. If one has enough CPF money to work with, cash payments for a new home will be minimal. This means potential homeowners only have to shell out dollar bills for the application fee and other miscellaneous payments. Now it’s time to crack heads over the perfect interior design work.