Financial Planning | Investing | Personal Finance | Article

Want to Double Your Money? Here’s How Long It’ll Take

by Sophia | 27 May 2021 | 4 mins read

Putting money in the stock market is a lot like putting something in the oven, except you don’t actually know what to set the timer to. If you put $5,000 in the “oven” today, do you know how long it’ll take before it turns into $10,000, or doubles?

So much of investing is about being patient, trying not to time the market, and just being consistent and disciplined about your approach. But we’d all probably sleep a little easier (and maybe become even more disciplined about investing!) if we could just figure out how many years it would take for our hard-earned money in the market to double.

Well, you can. You just need to understand the concept of compound interest, and something called the Rule of 72.

Compound interest: a brief definition

Compound interest is basically the interest rate on your principal amount (whether for your bank account deposits or investment in the market) in addition to the accumulated interest earned, year on year.

In other words, your money’s going to grow — and it’ll grow way faster in an investment product (or even your CPF special account!) that generates 4% returns p.a. than if you put it in a bank account with an interest rate of something measly, like 0.35%.

That’s easy enough to understand. But calculating your returns, year on year, with compound interest in the mix? People have tried (and failed) to create elaborate Excel spreadsheets to try and chart this growth.

Unless you’re a guru with mathematical formulas and love spending hours on end putting together a spreadsheet that will go on for days, let’s dive into something called the Rule of 72 to figure out just how long it’ll take for our money to double.

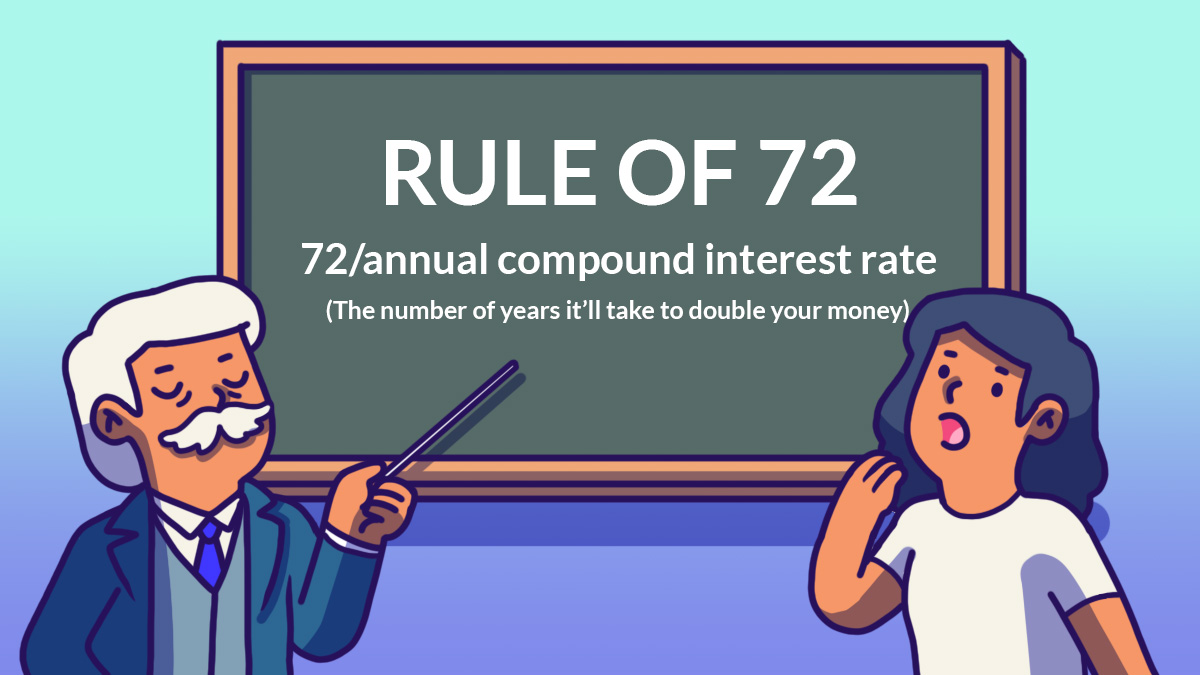

It’s elementary, Watson: Rule of 72

(72 / annual compound interest rate) = the number of years it’ll take to double your money

This is a simple equation that will likely follow you for the rest of your life as an investor. This will help you to estimate the number of years it will take for your investment to double in value.

Let’s take your CPF special account, for example. Your SA boasts a rate of return of 4%, year on year. This means that whatever money you put in there will grow at a compounded rate of 4%. Let’s say you currently have $15,000 in there right now, and you’re not earning any income to supplement the amount.

Using the Rule of 72, the equation goes something like this:

(72 / 4%) = 18

And voila! It will take you 18 years for that $15,000 in your CPF SA to turn into $30,000.

You can use this rule to guesstimate something else, like your investment portfolio’s value, assuming it maintains a steady rate of return.

This rule can also apply to inflation, by the way — to find out how long it will take before the value of your dollar is halved! So, even if you have $1 million in the bank right now, or in your investments, this is how long it will take for the value of that money to be cleaved in two, assuming an inflation rate of 2%.

(72 / 2%) = 36

Sure, 36 years is a long time, but that’s no reason to slack off.

In fact, the rule of 72 is useful because it gives you an actual timeframe to work with, so you can plan your investment or other money decisions within it. You can decide where you want to invest, or what you want to invest in, to net yourself a higher rate of return (and thus, reduce the number of years it’ll take for your money to double).

However, there’s a caveat to all of this: the rule of 72 gives you accurate results for low rates of return. If your rate of return is 20% or higher (which would be amazing in itself), the numbers may become skewed or inaccurate.

The thought of investing and saving for retirement might sound like a drag, but it might be because we’re unable to actually see the endpoint, or the moment where our efforts finally pay off.

By using the rule of 72, we’ll be able to see the future just a little bit more clearly, and perhaps feel more motivated to continually invest, and to make investing decisions that beef up our portfolio for a higher rate of return — to either retire on time, when we plan to, or to retire early and achieve FIRE.