Should you take a HDB or a bank loan? This is a question all Singaporeans face on the road towards homeownership.

But we will go through why we think getting a HDB loan just makes more sense — for your first home at least.

Yes, Bank Loans Have Been Cheaper

We know, we know, bank loans are undeniably the cheapest option. In the last decade, the interest rate on bank loans has been much lower compared to HDB loans.This is due to the low interest-rate environment that has been

set by Central Banks around the world. Because of this, banks have been able to offer attractive rates to entice over customers.

At this moment, bank loans can be around 0.5% lower than the HDB loan rate of 2.6%. This means on a $300,000 loan you are able to save around $1,500 per year.

But the real question is, will interest rates continue to be low in the coming years?

Nobody knows what the future holds, but we can look to the past for clues — comparing the historical rates of HDB loans against bank loans to see what the trend has been.

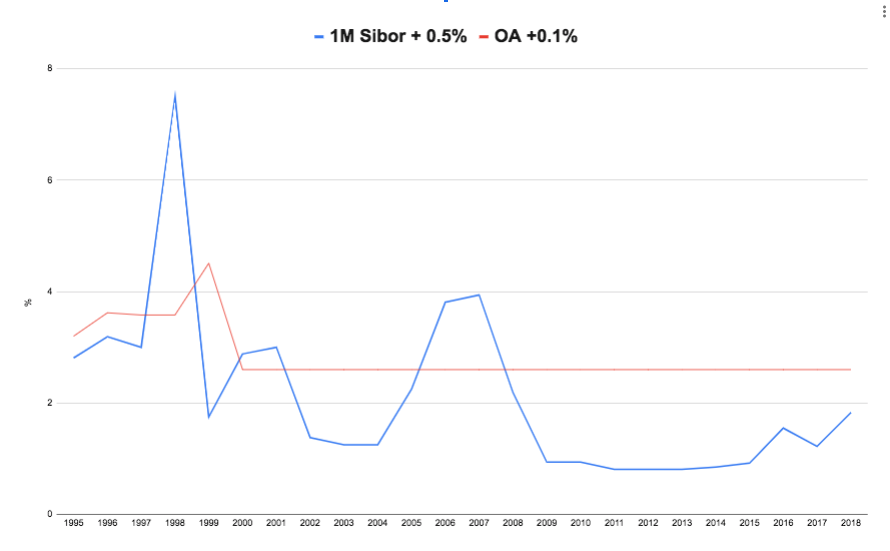

There are many types of loans offered by banks, but we will use 1M SIBOR pegged loans, the most simple and transparent type of bank loan because they reference SIBOR rates ∏— a

published interbank rate.

Atop this rate, we will also add another +0.5% to account for the bank’s profit.

We can see over this 25 year period between 1994 to 2018, bank rates have been largely lower than HDB’s (but note that in 1998, the 1M Sibor soared to 7%!).

Compared to this, HDB interest rates — pegged at 0.1% higher than the CPF’s Ordinary Account’s (OA) rates — has been flat (but higher than our bank loan) for most of the last 25 years. Notice that it too spiked up to 4.51% in 1999.

At this point, some of you might be surprised to learn that the CPF OA rate

can go up.

Although the CPF OA has been flat at 2.5% past decades, it does not mean that it will stay that way. This is because CPF OA rates are set by following a three-month average of the big three local banks’ interest rates, or the legislated minimum of 2.5% — whichever is higher.

Because interest rates have been so low, CPF OA rates have been at the legislated minimum of 2.5% for a long while now.

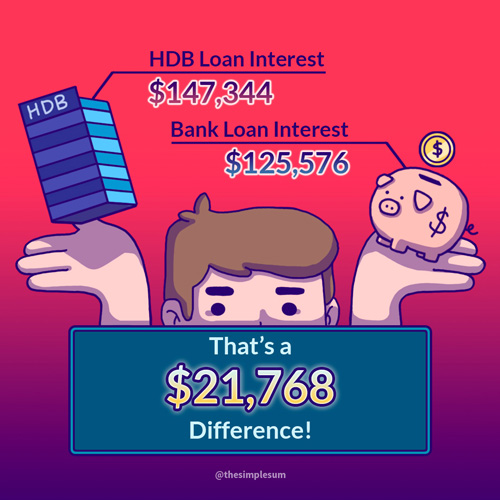

So let’s get down to it! Cost-wise, who wins? Charting a hypothetical repayment of a $300,000 loan through this period, a bank loan would have saved a couple

$21,768 in total interest payments over 25 years.

It seems the bank loan won hands down, so what was the point of all of this? Doesn’t this just prove that bank loans are better?

But take a hard look at that 7% figure. Can you handle it when your monthly payment suddenly spikes that high?

Most first-time homeowners would likely be in the early stages of their careers. A sudden spike in their loan repayments could cause cash-flow issues.

Not to mention they might be stressed, wondering what tomorrow’s rate may be.

So for some, it really just comes down to the simple ease of mind that a HDB loan provides. While both bank and HDB rates

will hike in tandem in a high-interest rate environment, but because HDB loans are pegged at 0.1% above the OA rate, you won’t feel you are ‘losing’ too much compared to your CPF OA savings.

Flexibility of HDB Loans

Let’s face it, banks are for-profit organisations. To earn the maximum profit, banks need to get you to stretch your loan with them as long as possible. The longer your loan tenure, the more interest they earn.

But what happens if you start to do better in the later stages in your career and wish to become debt-free? Perhaps by clearing your mortgage as soon as possible?

With banks, if you decide to make an early repayment, they will lose the opportunity to make money from you, so banks have early repayment penalties and will charge admin fees to process prepayments. You can be charged up to 1.5% in prepayment penalties if you prepay within the lock-in period.

Also, most banks only allow larger prepayment minimums — usually starting from $10,000.

Unlike banks, HDB is a statutory board whose main job is to provide affordable housing, so, turning a profit is not its main purpose. That’s why HDB allows you to make early repayments for your HDB loan, at any time, without penalties or admin fees.

Got a fat bonus? You could make an early repayment towards your flat, this shortens the duration of your loan and reduces the total interest paid, HDB prepayment minimums also start lower at $5,000.

Consider Your Cash-Flow

This one is a big one for young first-time homeowners. You are likely in your late-twenties, broke after paying off your wedding, but there are still incoming renovation and furnishing costs — simply put, you will be broke.

Taking a bank loan for your home means that you will need to fork out 25% of your home’s value in either cash or CPF downpayments.

So if your home costs $300,000, you will need to fork out $75,000 upfront — while most of it can be paid with CPF monies —

$15,000 or 5% of the loan must be in cash.

In contrast, a HDB loan only requires you to fork out 10% of your home’s value as a downpayment — and it can be wholly paid for with CPF.

Even if you could afford the cash downpayment, you are losing the opportunity to deploy that cash into investments early — missing out on compounding effects.

In Conclusion

Don’t get us wrong, bank loans can definitely save you a chunk of money, but that comes at a price — bank loans are simply much more complex products.

With bank loans, there are quite a lot of things to unpack, they have many different mechanics to understand — such as repricing and refinancing — these mechanics bring with them a whole host of unexpected legal and admin fees (and penalties) that can eat into the savings you made on the lower rates in the first place.

Which brings us to our last point, let’s say you started off with a bank loan, but you grow tired of the repricing and refinancing game and you want out!

The bad news is that you can’t — once you go bank, you can’t go back.

But if you started off with a HDB loan instead, you can refinance with a bank loan if you do decide to in the future.

In the end, we are not saying that bank loans are worse, but they require analysis and understanding before diving in.

If you are a first-time homeowner, it might be a better idea to dip your toes in the shallower end of the pool with a HDB loan.