So if you read this

first article, you would know that ETFs can be a good investment vehicle for average joe who never wants to figure out how equations like these work.[caption id="attachment_5898" align="aligncenter" width="530"]

funky math to analyse individual shares[/caption]

We will go through a popular plan that throws formulas like these out the window. Relying on broad index ETFs to create a

lazy investment portfolio for retirement investing.This route allows you to continue living life after work; Not going down the crazy rabbit-hole of stock-picking.

The 3-Fund Portfolio

An investment portfolio might sound

cheem. But it’s simply a bundle of different investments put together to meet one’s investment objectives. Additionally, a portfolio has rules in place that provides a framework for an investor to manage risk.

And here it is, the simple 3-fund portfolio:

- Local Shares ETF

- Global Shares ETF

- Local Bond ETF

Like a 3-aside soccer team, each plays a key role in your team to score – and reach your retirement goal.

Local Shares ETFs

This guy is the local striker in the team, doing the legwork and getting your money working in the high growth – but risky – shares market.

In Singapore, there is only one national index, which is the Straits Times Index (STI). Which tracks the performance of the top 30 SG-listed companies.

However in the recent years, Mr STI is moving slowly, he’s getting a bit pudgy, moving around sideways…

[caption id="attachment_5899" align="aligncenter" width="1024"]

STI – moving around indecisively[/caption]

The STI has had an average annual return of 3.71% per year (with reinvested dividends) – still higher than inflation – but not terrible sprightly.

Because of this flat performance, some prefer to look to more promising ETFs overseas.

[caption id="attachment_5900" align="aligncenter" width="1024"]

S&P 500 – onwards and upwards[/caption]

For example, observe the general upward trend of the American S&P 500. The U.S index that tracks the top 500 American-listed companies.

Over the last 5 years, it has returned 10.7%, almost 3 times more than our local index.

Holy cow!

Looking at this performance, should we ditch the STI altogether?

But the local hero still has an ace up his sleeve, the home-ground advantage. Because the STI is naturally denominated in SGD, it is not exposed to the risk of fluctuating currency exchange rates.

The older among us might remember that 20 years ago US$1 bought S$1.70. But today, the same U.S dollar gets you S$1.35. So keeping the local index on your team serves as a hedge against that risk. After all, if one retires in Singapore, they have to spend Singapore dollars.

This is especially important because if you are unlucky, and foreign currencies

crash upon your retirement, there will still be the locally priced investments to liquidate and rely on first.

Global ETFs

But still, that ×3 performance from the foreign funds is not something to be ignored. So when the local player is getting slow and fat – and you need to bolster your team’s performance – what should you do?

*Trigger warning*

Import fresh and exciting talent from overseas!

Diversifying into the

global economy moves your portfolio away from the risk of prolonged stagnation in the Singapore market. Or any single country’s market for that matter.

However, accessing global ETFs comes with a caveat: because the US is the strongest economy in the world, any global ETF cannot avoid being heavy on US companies.

The bad news: non-US investors will be slapped with a 30% tax on dividends distributed by U.S shares.

Some shares within the ETF pay dividends to reward owners (you), however for foreign investors, U.S listed dividends are heavily taxed.

There’s one way to reduce this – by buying global ETFs domiciled in Ireland (listed on the London Stock Exchange), which has a tax treaty with the USA, this halves the taxation to 15%.

The second drawback is that the foreign superstar is going to want to be paid in his home currency, the USD. Thus, you will be exposed to foreign currency risks.

Local Bonds

The last ingredient in the portfolio is the local bond fund. Think of bonds as the mature and level-headed goalie on your team.

By nature, bonds are considered less risky than shares. As

bonds are essentially loans provided by investors to companies or governments – these lenders have a commitment to pay back their debts (unless they go bankrupt of course, so having the bonds in ETF form diversifies away from this risk).

Because of this feature, bonds are more stable in prices.

During market dips and rises they do not swing as wildly as stocks, this is desirable especially when you are nearing retirement, and start selling your investments to fund your retirement expenses.

So in summary, in the first half of your life(wealth accumulation stage), your two strikers are let out to attack. But during the second-half (drawdown during retirement), bonds take the centre-stage in the defensive play, preventing losses and preserving your wins.

ETF Options

Here are some ETFs that fit the bill of what we outlined above.

Local ETFs that track the STI.

SPDR Straits Times Index ETF (ES3)

Nikko AM Singapore STI ETF (G3B)

Global ETF that has the Irish tax break:

iShares MSCI Core World (IWDA)

- Over 1,600 companies from 23 developed markets

- Bonus: This ETF is dividend accumulative, meaning fund managers automatically reinvest any dividends for you – essential for your investment to snowball faster.

Vanguard FTSE All-World (VWRA) *launched 23rd July 2019*

- Over 3,265 companies from 47 developed & emerging markets

- Bonus: This ETF is also dividend accumulative, meaning fund managers automatically reinvest any dividends for you – essential for your investment to snowball faster.

Two local bond fund options:

ABF Singapore Bond Index Fund (A35)

- Basket of bonds from the Singapore government and other government entities, HDB, URA, LTA, etc.

- Government bonds are generally considered the safest.

Nikko AM SGD Investment Grade Corporate Bond (MBH)

- Basket of bonds from large local companies such as SIA, HSBC, Starhub, etc.

- Higher growth, with slightly more risk of default.

This list is not exhaustive, there are many other options available in the market for Global ETFs. On the local front, the bond component can even be substituted with the ever-popular Singapore Savings Bonds (SSBs).

Investment Portfolio Allocation

But how then do you set up the team formation? 1-1-1? 2-1? 1-2? In other words, if you have $1,000 a month to invest with, how do you split your cash between the three funds?

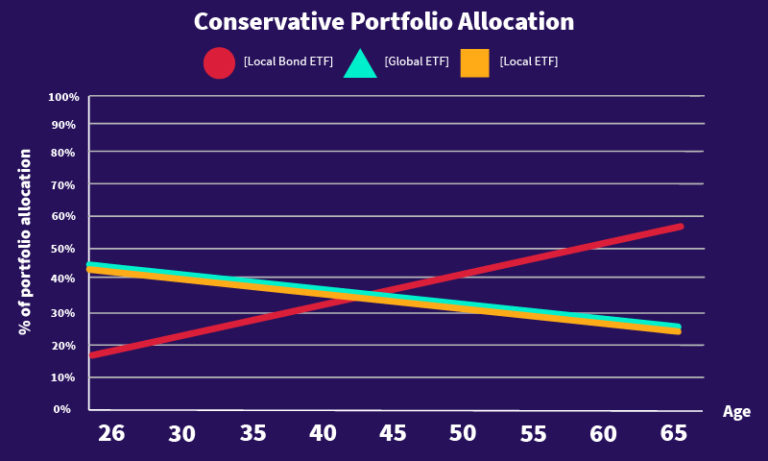

More conservative portfolio allocation strategy

A rule of thumb would be to use the

110 less your current age equation to determine shares allocation, the rest will be put into the bond fund.

For example, if an investor is 26 years old. The answer would be 84% of their portfolio into shares, then further split, equally between local and global share ETFs. The other 16% will be put to the bond fund.

[Local Bond ETF] 16%

[Global ETF] 42%

[Local ETF] 42%

The rationale is that when one is younger, they can afford to take more risks with higher growth shares. But as they age, the allocation slowly shifts towards wealth preservation with bonds.

But why the 110 figure?

At older ages, there should still be a decent portion of your investments in shares, to help your pot of gold combat inflation and regenerate itself.

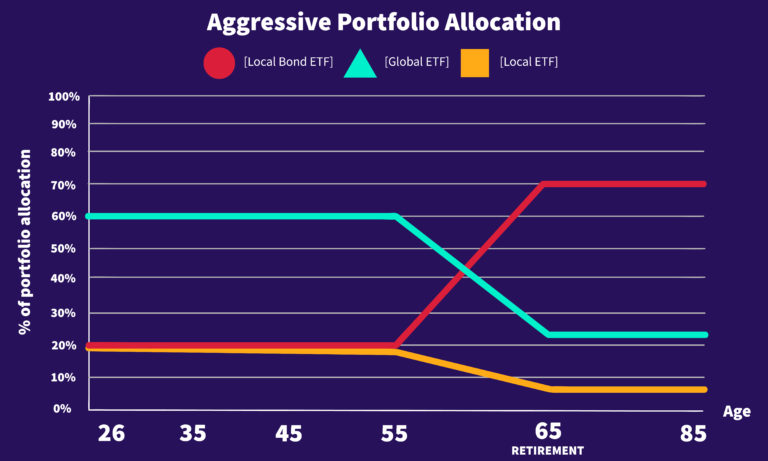

Aggressive Portfolio Allocation

However, for those who are looking for a more aggressive portfolio during their working years, they could choose a fixed 80/20 share to bond allocation like this:

[Local Bond Fund] 20%

[Local ETF] 20%

[Global ETF] 60%

This portfolio is weighted in favour of the more dynamic global shares. This fixed ratio continues until 10 years before retirement. Gradually tilting towards a more conservative 30/70 share to bond ratio, where it stays fixed during throughout your retirement years.

Rebalancing

Okay, remember we said that this strategy is for people who wish to set-it and forget it?

Well, we lied. Only slightly though.

There’s

some work to do, but the good news is that you only really need to do it twice yearly. This is for you to review the performance of your stocks and bonds and rebalance them.

What is rebalancing? Well, perhaps after a year of investment, the Global ETF portion has done exceptionally well – the star player in your portfolio so to speak – outshining the rest.

If we used the example of the 60/20/20 allocation rule. The global ETF portfolio would have broken out of its 60% ratio.

So what an investor should do is to rebalance the portfolio to bring it back to its original targets. In this instance, selling off the winning global ETFs, and distributing the profits to the other two laggards, bringing the components back on target.

[caption id="attachment_5906" align="aligncenter" width="768"]

perfectly balanced, as it should be[/caption]

This is a systematic way for you to realize profits off good performers, and channel said profits into portfolio components performing less well.

In essence, selling high and buying low —

though according to history this is 50/50, sometimes you could be prematurely selling your stocks that could rise higher if you let it be — but according to historical data, even then, it would not impact the returns of your portfolio that much.

The offshoot benefit of this is that the 2 times a year you rebalance your portfolio, is also be the perfect time to reinvest the dividends distributed by your local ETFs.

Reinvesting Dividends

As mentioned, the IWDA ETF and VRWA ETF in the global category automatically reinvests its dividends. Unfortunately, this feature is not generally available for the local indexes.

The local share indexes distribute their dividends twice-yearly, while the bond ETFs distribute once, in January. Here are the typical distribution dates for the local ETFs.

Dividend distribution date for STI ETFs

Nikko STI – Jan & July

SPDR STI – Feb & August

Bond ETFs

MBH & AB3 – Jan

So depending on which STI fund an investor has, they can choose the designated rebalancing dates to be just after these dividend payout periods. Perhaps

Jan and July. Strategically chosen to reduce the amount of effort needed, yet redeploying their money back into the market ASAP, making their money work for them!

Smart and lazy. Perfect.

Stick around for the last article in this series, outlining this lazy man’s investment strategy, we will go through which brokerages and banks you can use to purchase these ETFs.

The final part of the series can be found

here.

This article does is not investment advice, please your own due diligence to ensure an investment or an investment strategy is right for you.